Annually since 2005, McKinsey has analyzed the aviation value chain.

We look at participants from across the value chain, including airlines, aircraft and engine original equipment manufacturers (OEMs), aircraft lessors, air navigation service providers, jet fuel producers, airports, catering suppliers, ground services companies, maintenance, repair, and overhaul (MRO) organizations, freight forwarders, and providers of global distribution systems and other travel technologies. We analyzed the financial performance of the aviation value chain through the lens of economic profit, defined as the difference between the return on invested capital (ROIC) and the weighted average cost of capital (WACC).

Below is a brief snapshot of our findings. You can access the full analysis.

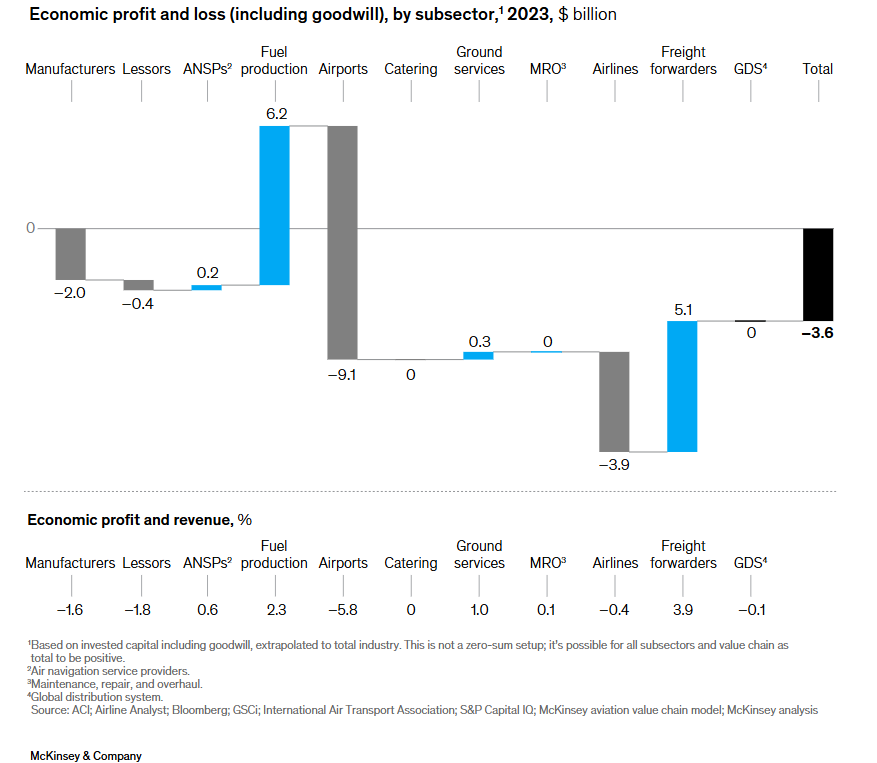

Our newest results, based on 2023 data, indicate a strong year in which nine of the 11 subsectors we track improved, compared to 2022 levels. The aviation value chain achieved a significant recovery, recording a marginal 2023 economic loss of roughly $3.6 billion compared with its 2022 loss of an estimated $67 billion. The overall results supported by the ongoing recovery in air travel, represent a significant improvement compared with 2022.

Beneath the surface, there have been notable shifts.

The airline sector, though still marginally negative in terms of economic profit, notched its best performance in decades and featured the highest proportion of value-creating airlines that we have observed in the history of this analysis. Jet fuel producers, which benefited from elevated fuel prices, and freight forwarders, which continued to see strong air cargo demand, achieved the largest profits. Airports, airlines, and OEMs suffered the largest losses in absolute terms.

Drilling down within these subsectors reveals a few narratives. For instance, disruptions to aircraft production supply chains have created both challenges and opportunities. OEM production levels remain materially reduced, and aircraft and engine OEMs as a group generated economic losses of about $2 billion in 2023. But fewer new aircraft being delivered amid strong demand means that airlines are extending the service lives of their existing aircraft: the share of commercial fleet aircraft that are 25 or more years old increased to 9.6 percent, from 8.1 percent. Older aircraft require more maintenance, so the MRO sector rebounded to modest economic profitability of about $42 million (equaling roughly 0.1% of revenue).

Meanwhile, in cargo—one of the few bright spots for aviation during the pandemic—demand remained strong, propelled by e-commerce orders. Capacity also rebounded, aided by increased availability of wide-body aircraft, which led to cargo yields dropping by approximately 32%, but still above pre-pandemic levels. In 2020, the only value-creating airlines were all-cargo airlines, but by 2023, all-cargo airlines constituted only 2% of value-creating airlines. Freight forwarders continued to generate the largest economic profit of any subsector in absolute terms (about $5.1 billion in 2023), but results were down from the previous year’s profit (about $7.2 billion in 2022).

The full analysis and dives deeper into the various aspects of the performance of the aviation value chain.

Authors:

![]()